The environmental crisis has drawn people’s interest in alternative energy sources. In the last decade, the most investment in PV manufacturing was seen in some of the major world powers such as the United States, China, Europe, and Japan.

Only between 2006 and 2007, there was a 50-percent increase in cumulative installed capacity reaching approximately 7.7GW.

Nonetheless, there are a few bumps on the road for solar energy development projects. While solar energy and other renewable energy systems have shown improvement during the past decades, some global factors threatened this growth.

Before the Covid-19 pandemic, Rystad Energy predicted a 140-gigawatt addition in the industry in 2020. This corresponded to a steady growth history of 15% on a year-to-year basis.

Nonetheless, the pandemic hit, and the landscape changed completely. Back in March 2020, experts predicted a harsh period for renewable-source projects. On the verge of what may be the highest recession in modern history, the outlook for innovative enterprises did not look good.

During a recession, several factors affect the PV manufactory industry and the solar energy projects in general.

Factors and conditions that affect the PV manufacturing industry

Lack of financing

During a recession, the liquidity levels are lower, hence the market shrinks. With less liquidity out there, there is less money to be put into projects. Moreover, investors tend to move their allocations into safe assets like fixed-income vehicles withdrawing their investments from riskier industries.

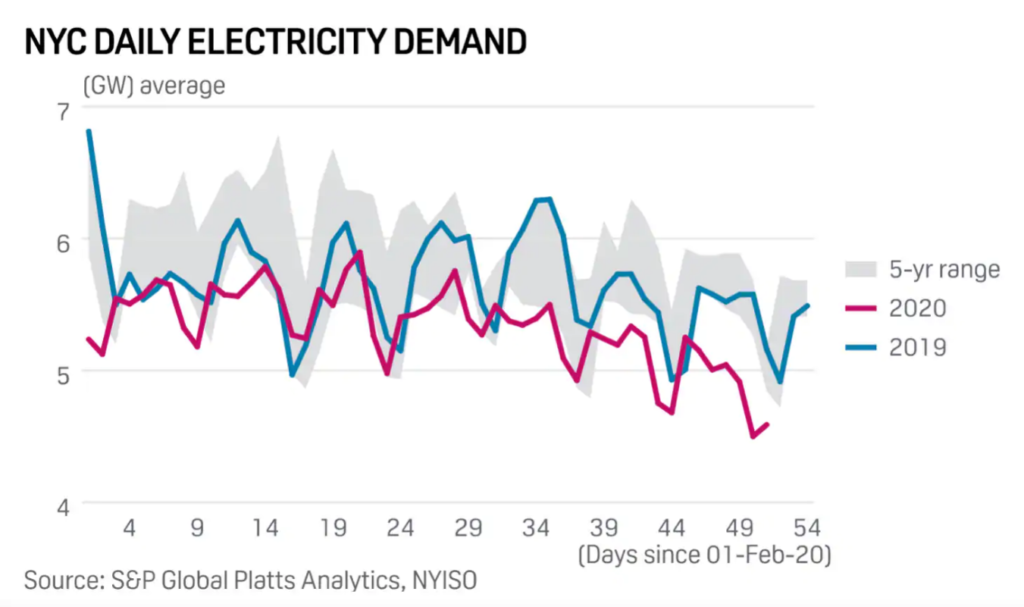

Low electricity demand

As large investors tend to be cautious and withdraw their capital from less traditional markets, average citizens tend to spend less. This impacts energy consumption (like shown in the chart below) hence affects energy markets.

Although the renewable energy sector is protected by PPAs (Power Purchase Agreements), these prices are usually higher than market prices, which can also draw investors away.

Stranded projects

In line with the previous point, small or newly released projects may never see the light of day. Financing is arguably impossible to get in such a context and, even if self-financed, a project owner may find other challenges. The cost of the materials increases and is usually in US dollars, which makes it difficult for projects that work with other currencies. In a recession, currency volatility can make it impossible for a project to face exchange costs.

This has been worsened during the coronavirus crisis due to transportation restrictions that generate even greater costs and involve delays.

Sources indicate that, since March 2020, there was a shortage of materials like inverters and modules which resulted in a 15-percent increase in prices.

The renewable energy industry during the Covid-19 pandemic

Besides the negative predictions, the renewable energy industry is throwing good results in 2021. In April, the IRENA (International Renewable Energy Agency) released encouraging reports. IRENA’s statistics show an increase in new generating capacity for the second year in a row. It reports a growth of 260 gigawatts in renewable energy capacity in 2020, exceeding 2019 almost by half.

This increase has taken place partly due to the underperformance of the fuel-energy sector. There was a net decommissioning of fossil power generation in Europe, North America, and Eurasia. This sector saw a decrease from 64 GW to 60 GW in 2020, in line with an overall bearish tendency.

Solar energy, in particular, is a worthy player in this increasing curve. It has reached nearly the same level as wind capacity. This is thanks to the expansion in Asian countries with a 45 GW increase in China and 11 GW in Vietnam. Japan added 5 GW while India and Korea added 4 GW. The United States increased its capacity by adding 15 GW.

Total solar capacity has reached practically the same level as wind capacity in 2020

PV module manufacturers, the most important industry players in 2020

The PV manufacturing industry has shown interesting tendencies. For a while now, a small group of players has controlled the polysilicon and monocrystalline wafer manufacturing. This consolidation is still growing, and this is reflected in statistics from the past years.

The market for module and cell construction has been historically more fragmented, however, this tendency is changing. While smaller participants used to take part in this niche, in 2020, their involvement seemed to be decreasing.

Some of the Chinese biggest players in the industry are taking over the module and cell construction markets. This is partly because the industry is gradually starting to use larger wafer formats, hence, small companies cannot afford the building costs. This opens the way for the PV industry giants, who have the means to build the wafers that the current market demands.

The next section presents an analysis of today’s PV manufacturing industry and how to evaluate the manufacturers’ competency in this context.

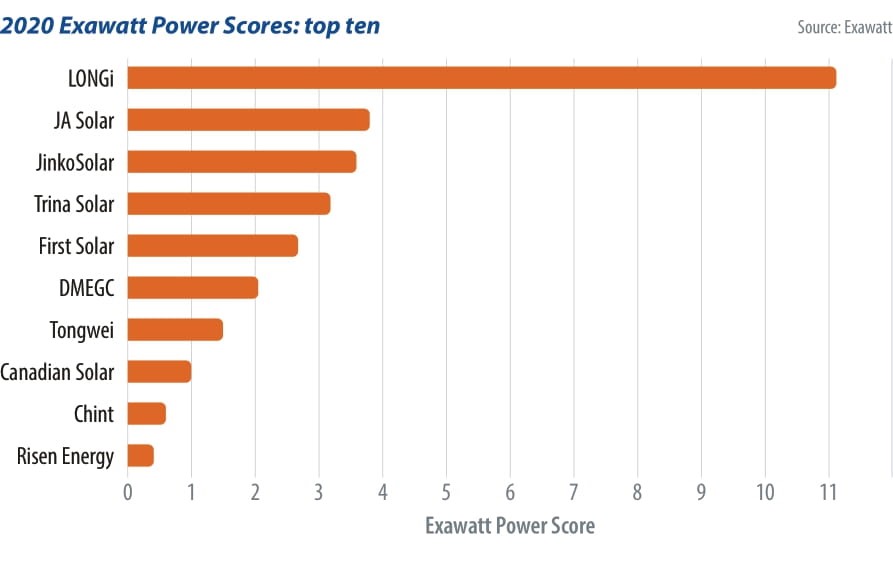

The graphic shows the top ten PV manufacturers in 2020 according to Exawatt

How to measure and compare PV module manufacturers?

But how do we compare different market players based on parameters other than capacity and shipment? Fortunately, Exawatt has developed a ranking (Exawatt’s Power Score and Power Ranking) to compare different module builders in the market. Nonetheless, a company’s place in this ranking does not necessarily reflect the quality of its products.

The ranking is based on three parameters: PV presence, financial health, and profitability.

Exawatt’s Power Source and Power rankings parameters

- PV presence:

This point is assessed considering the module shipment and capacity growth over a

certain period. It has a value of ‘2’ in the ranking.

- Financial Health:

This parameter is measured with the Altman z-score. It is used to forecast the probability

for a company to go bankrupt in the next 2 years. This parameter is worth 1 point.

- Profitability:

This point is assessed with two parameters: operating profit as a percentage of revenue

and interest expense as a percentage of revenue in a trailing 12-month period. This

parameter is also worth 1 point.

The top 5 industry players according to Exawatt’s Power Source and Power rankings

The Exawatt ranking’s results don’t surprise those who know the industry. Like we can see in the chart above, Longi is sitting in the first place having a leading position in the three parameters. Longi is not only known for being the largest manufacturer in the world but also has a strong financial and profitability position.

Longi has the largest capacity and shipment and boasts a healthy financial environment thanks to its rich wafer production. They have a significant wafer business and use their own wafers to build modules. This helps the company to reduce costs and remain competitive. Its operating margin was impressive even in the year of the coronavirus breakout. In 2020, Longi had an operating margin twice as large as that of many major Chinese manufacturers.

The second place was earned by JA Solar, the only manufacturer (other than Longi) to achieve a positive score in all three parameters. Its PV presence was boosted by the company’s major expansion regarding shipment and capacity.

The ranking is followed by Jinko Solar, Trina Solar, and First Solar (third, fourth, and fifth place respectively). First Solar is one of the few Western PV manufacturers in the ranking. Its strongest parameters are profitability and financial health.

DMEGC is in sixth place, which may come as a surprise to many. However, although its manufacturing levels are low (1.5 GW capacity in 2020), the company shows a robust position when it comes to financial health and profitability.

In both parameters, DMEGC ranks quite higher than most competitors and this is mainly thanks to the company’s devices business and magnetic materials. These features are highly coveted by investors and thus significantly improve DMEGC’s market capitalization.

Longi leads the ranking with the largest capacity and shipment volumes in the market

Exawatt’s Power Source and Power rankings: top 5 positions

- Longi

- JA Solar

- JinkoSolar

- Trina Solar

- First solar

Players looking for a brighter future

The ranking brings yet another surprise with two of the most reputable companies in the PV module industry in the lowest positions. GCL System Integration and Talesun are positioned in the 29th and 30th places from the 31 companies appearing on the ranking. Both companies scored negative points in all three parameters and position themselves below the overall average.

GCL reached a sales level amounting to nearly 3 GW in 2020, which is 17% less than in 2019 and 50% below the company’s highest sale point in 2018. This consolidates a decreasing trend in its performance and creates a negative score for the PV presence parameter.

Despite being underutilized (GCL had a capacity of 7 GW in 2020), the company has expansion plans. There is a 15 GW module manufacturing facility due to come online this year.

Talesun is in a similar situation having shipped only 1.3 GW in 2020 (25% less than 2019). Nonetheless, the company recently added 5 GW of module capacity online, reaching a total capacity of 13 GW.

Thanks to these expansions, both companies will be able to build larger modules. Since the whole industry is shifting to the use of larger cells and wafers, this brings hope for GCL and Talesun. Maybe these conditions will help them climb a few positions in the Exawatt ranking for 2021.

Predictions for this year

Many PV module manufacturers are planning to expand their capacities in 2021 which may change the game for some of the main players.

Jinko Solar, for example (currently on position number three), may fall a few places. This is because JA Solar (2nd place) and Trina Solar (4th place) are planning major capacity expansions. If these plans turn out to be successful, both companies can increase in presence and profitability thus pushing Jinko out from the top three.

But these are not the only manufacturers with expansion plans for 2021. Canadian, Elsewhere, and Risen Energy are some of the companies that may climb the ranking by improving module capacity. Nonetheless, if Longi achieves its objectives this year and reaches the targeted 40-GW module shipment level, chances are it will remain the undisputed leader.

It is widely known that the Covid-19 pandemic has affected the markets since March 2020 and its effects are still visible in 2021. The PV module industry is not the exception. Due to the numerous travel and movement restrictions, shipping costs have increased and are likely to continue like this for the rest of the year.

This may result in fragmentation and localization of a market that has been mainly controlled by Chinese players. This could mean the entrance of new companies in 2021’s ranking, particularly from module manufacturers.

How N-type transition may influence the market in a near future

Exawatt’s experts are also considering the market’s major trends and their possible impact. From early 2019, they have predicted that n-type TOPCon and HJT technology would approach a cost-per-watt parity with p-type mono PERC in a near future. This would mean a major shift similar to the transition from BSF to mono PERC.

In 2021, the market keeps showing a TOPCon and HJT trend. Both small and large players are moving towards this technology. While small manufacturers are trying to make a difference and get a better position in the market, big companies are conducting pilot tests before launching mass-scale production.

In this context, we need to wait and see if the non-Chinese greatest brands like Panasonic or LG Electronics will be able to maintain a differentiating factor while their Asian counterparts transition towards TOPCon and HJT technology.

In the same line, we can ask ourselves whether early innovators in the n-type cells (like Jolywood) will thrive or be overshadowed by the usual industry leaders.

Also, the companies that move down the HJT road will have the opportunity to capitalize on the requirements for entirely new cells. This would create a more fragmented market and may pave the way for new companies to enter the rankings in future years.

PV manufacturers in 2021, a conclusion

The PV industry is facing many challenges in the post-Covid-19 world. Yet, as some things change, others remain stable.

The third decade of this century has brought unpleasant surprises. Shipment and polysilicon prices are volatile, and costs are increasing. Moreover, in times of recession, the demand for energy services is usually lower and the investors’ confidence is diminished. Thus, it becomes harder for smaller projects to find financing and the big companies see their prices fall in the market.

But one thing seems to be consistent, and this is the global tendency towards a more sustainable future with the help of renewable energy sources. Installations are growing, companies are expanding their capacity, module efficiency continues to improve and, most importantly, innovations continue.

At the same time, some factors bring further uncertainty into the PV manufacturing industry. The movement towards new technologies, the increasing use of larger wafers, the fragmentation tendency due to movement restrictions and high shipping costs may change the ranking’s layout in a not-so-distant future. There is also a high probability that the strongest players will continue to lead the way of innovation while the industry grows into developing highly efficient energy sources.

References

https://www.sc.com/en/trade-beyond-borders/covid-19-clean-energy-challenges-and-opportunities/

https://www.renewableenergyhub.co.uk/main/solar-panels/solar-panel-manufacturers-and-products/